*Originally published on CUInsight.com

“Payment services hub” or “payment hubs” used to mean a consolidation of systems supporting Fedwire and ACH processing, which helped large financial institutions bring together their Commercial and Retail payment operations. Payment systems were historically introduced one at a time as new payment methods became available, giving rise to silos by workstream for operations such as product management, customer service, compliance, etc. for each payment type. An example of this is check processing, which began in the 1950’s.

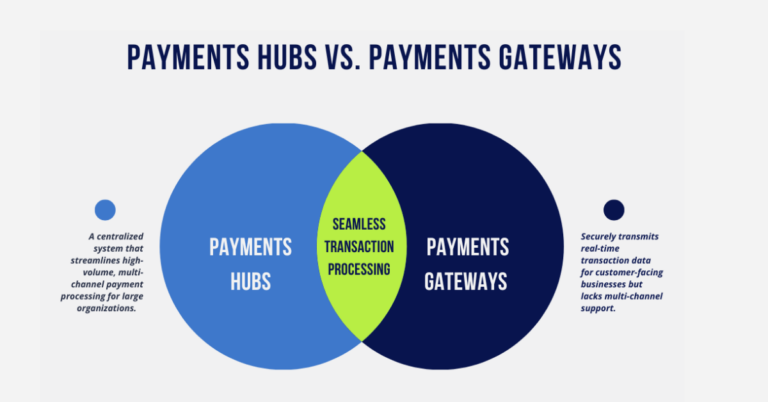

Today, “payment hub” has expanded to include new real-time payment rails such as TCH RTP® network, the FedNowSM Service, and reverse debit networks such as Visa Direct and MasterCard Send. Celent refers to payment hubs as ‘where a single solution can process all payments on a single platform’.

Here is how the payments services hubs of today are different:

- They are no longer just for large financial institutions with large budgets – payments hubs used to have a million dollar price tag. The new generation of payments hubs are cloud-based, allowing financial institutions to scale and pay for what they need at a price they can afford.

- They are off-prem – a modern payments hub is not located on-prem. Instead, it’s located on a cloud service. However, this doesn’t mean that financial institutions can’t keep their existing services on-prem. In fact, they can actually combine what they have with the modern payment services hub.

- Not reliant on the core – previously, payments hubs were typically reliant on a particular core, making it necessary to replace the bank or credit union’s core payment processing capabilities. This made them totally reliant on their Core Provider for all transaction types. Financial institutions can now connect to modern payment hubs, regardless of core, making it possible to access faster timelines and better roadmaps. This also opens up a multitude of vendor opportunities and innovative solutions they would not have had previously.

- Smart routing capabilities – smarter, faster payments means automating the process of choosing which rails various payments transact on. This means the least expensive rail for the speed needed is chosen for the delivery of the payment.

- More benefits – financial institutions benefit from better reporting and analytics, improved user experience, streamlined functions such as regulatory compliance, and a faster time to market for new payment options.

Today, payment hubs are being used around the world at hundreds of banks, and most of the top 30 U.S. banks have at least one payment hub. They are a key component of payment modernization, and widen the gap between bank and credit union capabilities.

Learn more about payments hubs in Payment Services Hub Explained.

Alacriti’s centralized payment platform, Orbipay Payments Hub, provides innovation opportunities and the ability to make smart routing decisions at the financial institution to meet their individual needs. Financial institutions can take full ownership of their payments and control their evolution with ACH, Wire, TCH’s RTP® network, Visa Direct, and the FedNowSM Service, all on one cloud-based platform. To speak with an Alacriti payments expert, please contact us at (908) 791-2916 or info@alacriti.com.